By going through these Maharashtra State Board Class 12 Economics Notes Chapter 4 Supply Analysis students can recall all the concepts quickly.

Maharashtra State Board Class 12 Economics Notes Chapter 4 Supply Analysis

Terms related to Production and Supply:

→ Producers undertake the production of goods and services which earn profit from them. They supply more goods and services at a higher price to earn profit. Like demand, supply is related to price and is also an important factor that determines the market price. Demand and supply are interrelated aspects of the market.

→ Supply is the outcome of stock and stock is the outcome of production. So, it is important to understand supply and its related concepts like production, stock, supply, etc.

→ Production implies the creation of utility, with the help of land, labour, capital, and organization. Production results in an output of goods.

→ Output is the outcome of the process of production in a given time in the economy with the help of factor inputs.

→ Stock is the total quantity of commodity available to the producer for sale at a point in time. Stock determines potential supply.

→ Reservation price is the seller’s minimum price below which the seller is not willing to sell even a single unit. If the market price is more than the reservation price then the seller will be willing to offer his stock for sale from his stock and vice versa. Usually, reservation price is low in the case of perishable goods and high in the case of durable goods.

Definition of Supply:

Supply in defined as “the quantities of a commodity that a seller is willing and able to offer for sale at a given price, during a certain period of time”. He sells more at a higher price and less at a lower price. Supply analysis may be of individual supply or market supply.

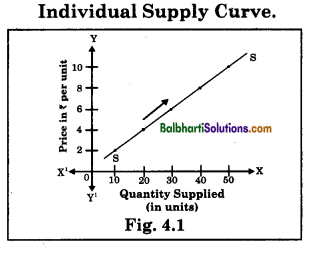

Individual Supply:

It refers to various quantities of a commodity an individual seller or producer is willing to sell at different prices. This can be shown by the individual supply schedules.

![]()

Individual Supply Schedule: It is a tabular representation of various quantities of a commodity that produce is willing to offer for sale at different prices during a given period of time as shown below.

| Prices of Commodity ‘X’ (₹) | Quantity Supplied per day (units) |

| 2 | 10 |

| 4 | 20 |

| 6 | 30 |

| 8 | 40 |

| 10 | 50 |

Individual Supply Curve: It is a graphical representation of an individual supply schedule. It slopes upwards from left to right showing direct relationship between price and quantity supplied as shown on next page :

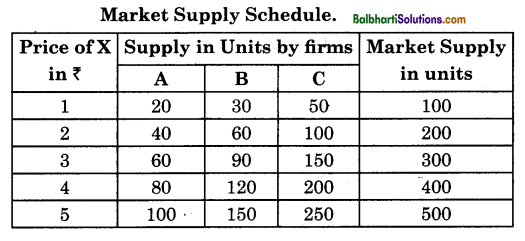

Market Supply:

It is the sum total of individual supply. It refers to various quantities of a commodity offered by all the sellers for sale at different prices during a given period of time. It can be shown by market supply schedule or market supply curve.

Market Supply Schedule: It is a tabular representation of various quantities of a commodity offered for sale by different sellers at different prices during a given period of time. It is obtained by horizontal summation of all individual supply as shown below.

![]()

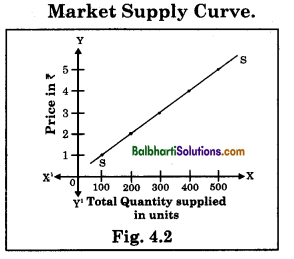

Market Supply Curve: It is a graphical representation of market supply schedule. It slopes upwards from left to right indicating direct relationship between price and quantity supplied as shown below.

Determinants of Market Supply:

→ Price of the Commodity – Price increases, Supply decreases and vice versa.

→ Cost of Production – Cost of Production increases – Supply decreases and vice versa.

→ Technique of Production – Advanced technology, Supply increases and Outdated technology, supply decreases.

→ Government Policy – Favourable government policy, supply increases and vice versa.

→ Exports and Imports – More exports, supply decreases, more imports, supply increases.

→ Future expectation – Fall in price expectation, supply decreases and vice versa.

→ Climatic Conditions – Favourable climatic conditions, supply increases and vice versa.

→ Nature of Market – Short period market, supply decreases, Long-period market, supply increases.

→ Infrastructure Facility – Well connected infrastructure, supply increases and vice versa.

→ Price of other goods – Price of substitute goods increases, supply increases, and vice versa.

→ Natural and Man-made Calamities – Natural calamities, reduction in supply.

Law of Supply:

According to Prof. Alfred Marshall, “Other things remaining constant, higher the price of the commodity, greater is the quantity supplied and lower the price of the commodity, smaller is the quantity supplied. ”

In other words, quantity supplied of a commodity varies directly with price.

Symbolically, it is expressed as S = f (P) [S = Supply, P = Price, f = Function of]

The law can be better understood with the help of a market supply schedule and market supply curve.

Market Supply Schedule: It is a tabular representation of various quantities of a commodity offered for sale by different sellers at different prices during a given period of time. It is obtained by horizontal summation of all individual supply as shown below.

![]()

Market Supply Curve: It is a graphical representation of market supply schedule. It slopes upwards from left to right indicating direct relationship between price and quantity supplied as shown below.

Assumptions of the Law of Supply:

- No change in Cost of Production

- No change in Technique of Production

- No change in Weather Condition

- No change in Government Policies

- No change in Transport Cost

- No change in the quantity of goods kept for self-consumption

- No change in Price of Competitive goods

- Constant Scale of Production If all these factors do not change, then more will be supplied at higher price and vice-versa.

![]()

Exceptions to the Law of Supply:

In following cases, more may not be supplied at higher price and vice-versa.

- Labour supply

- Savings

- Future expectations

- Urgent need for cash

- Rare goods

- Agricultural goods

- perishable goods

Variation in Supply:

When quantity supplied of commodity changes due to change in its price, other factors remaining constant, it is known as Variation in supply. It can be of two types :

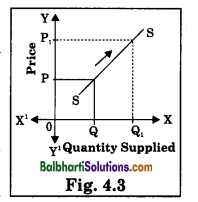

(A) Expansion or Extension in Supply : When quantity supplied rises due to an increase in the price of a commodity, other factor remaining constant, it is called expansion or extension in supply. It is shown by an upward movement on the same supply curve.

When price rises from 0P to 0P1 supply in the market also rises from 0Q to 0Q1( Hence it is shown by upward movement on the same supply curve.

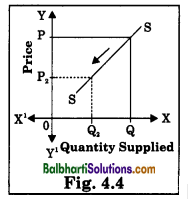

(B) Contraction in Supply : When quantity supplied falls due to fall in the price of a commodity other factors remaining constant, it is called contraction in supply. It is shown by downward movement on the same supply curve.

When price falls from 0P to 0P2, supply in the market also falls from 0Q to 0Q2. Hence this is shown by downward movement on the same supply curve.

Changes in Supply :

When the quantity supplied of a commodity changes due to factors other than price, it is known as change in supply. It can be of two types :

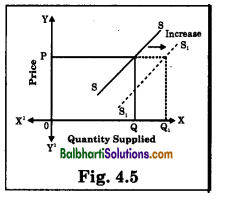

(A) Increase in Supply : When more quantity is supplied at the same price due to changes in factors other than price, it is called increase in supply. It takes place when, there is decrease in price of inputs, more imports, technological up gradation, fall in taxes, etc. It is shown by shift of the supply curve to the right of original supply curve.

When at the same price 0P, quantity supplied rises from 0Q to 0Q1 it is called increase in supply.

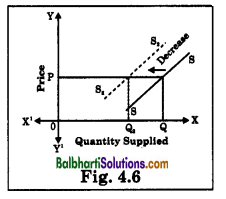

(B) Decrease in Supply : When less quantity is supplied at the same price, due to change in factors other than change in price it is called decrease in supply. It takes place when there is increase in price of inputs, old technological, more taxes, etc. It is shown by a shift of the supply curve to the left of original supply curve.

When at the same price 0P, quantity supplied falls from 0Q to 0Q2, it is called decrease in supply.

![]()

Concepts of Cost and Revenue :

(A) Concept of Cost: Cost of production means the aggregate money expenditure incurred by a firm on various inputs like land, labour, capital, etc. in the form of rent, wages, interest, transport, insurance, etc. There are three main types of cost TC, AC and MC.

Total Cost (TC): It is the total expenditure incurred by a firm on the factors of production required for the producing of goods and services. It is the sum total of Total Fixed Cost (TFC) and Total Variable Cost (TVC). Hence, TC = TFC + TVC

- Total Fixed Cost (TFC):

It is the cost incurred on fixed factors of production like land, factory, building, capital, etc. - Total Variable Cost (TVC):

It is the cost incurred on variable factors like labour, raw material, electricity, etc.

Average Cost (AC): It refers to per unit total cost of production. It is obtained by dividing Total cost by number of units of that commodity produced.

Hence, AC = \(\frac{\mathrm{TC}}{\text { Total output }}\)

Marginal Cost (MC): It is net addition made to the total cost by producing one more unit of output.

Hence, MCn = TCn – TCn -1 (n = Number of unit produced)

(B) Concept of Revenue :

Revenue refers to the amount received by a firm from the sale of given quantity of commodity in the market at different prices. Hence, Revenue = Price x Quantity Sold

The concepts of Revenue consists of three types :

- Total Revenue (TR),

- Average Revenue (AR),

- Marginal Revenue (MR).

![]()

Total Revenue (TR): Total Revenue refers to total receipts of the firm from its sales of commodity. It is obtained by multiplying the price per unit of the commodity with total number of units sold.

Hence, TR = Price x Quantity Sold

Average Revenue (AR): It refers to the revenue per unit of the commodity sold.

Hence, AC = \(\frac{\mathrm{TR}}{\text { Total quantity sold }}\)

Marginal Revenue (MR):

Marginal revenue is the net addition made to TR by selling an additional unit of the commodity.

Hence, MRn = TRn – TRn-1 (n = Number of units sold).