Balbharti Maharashtra State Board 12th Commerce Book Keeping & Accountancy Solutions Chapter 4 Reconstitution of Partnership (Retirement of Partner) Textbook Exercise Questions and Answers.

Maharashtra State Board 12th Book Keeping & Accountancy Solutions Chapter 4 Reconstitution of Partnership (Retirement of Partner)

A. Select the most appropriate alternatives from those given below and rewrite the sentence.

Question 1.

The profit or loss from revaluation on retirement of partner is shared by ______________

(a) the remaining partners

(b) all the partners

(c) only retiring partner

(d) bank

Answer:

(b) all the partners

Question 2.

Descrease in the value of assets should be ______________ to Profit and Loss Adjustment Account.

(a) debited

(b) credited

(c) added

(d) equal

Answer:

(a) debited

![]()

Question 3.

The balance of the capital account of retired partner is transferred to his ______________ account if it is not paid.

(a) loan

(b) personal

(c) current

(d) son’s

Answer:

(a) loan

Question 4.

Gain ratio = ______________ Ratio less Old Ratio.

(a) New

(b) Equal

(c) Capital

(d) Sacrifice

Answer:

(a) New

Question 5.

New Ratio = Old Ratio + ______________ Ratio.

(a) Gain

(b) Capital

(c) Sacrifice

(d) Current

Answer:

(a) Gain

Question 6.

Apte, Bhate and Chitale are sharing 1/2, 3/10, and 1/5 if Apte retire their new ratio will be ______________

(a) 5 : 2

(b) 3 : 2

(c) 5 : 3

(d) 2 : 5

Answer:

(b) 3 : 2

B. Write the word, term, phrase, which can substitute each of the following statement.

Question 1.

Credit balance of Profit and Loss Adjustment Account.

Answer:

Profit on Revaluation Accounts

Question 2.

The ratio in which the continuing partners are benefited due to retirement of partner.

Answer:

Gain Ratio

Question 3.

Debit balance of Revaluation Account.

Answer:

Loss on Revaluation

![]()

Question 4.

The ratio which is obtained by deducting Old Ratio from New Ratio.

Answer:

Gain Ratio

Question 5.

Money value of business reputation earned by the firm over a number of years.

Answer:

Goodwill

Question 6.

Partner’s Account where Loss or Profit on revaluation is transferred.

Answer:

Capital/Current Account

C. State whether the following statement are true or false with reasons.

Question 1.

Gain ratio means New ratio minus Old ratio.

Answer:

This statement is True.

As per definition, profit sharing ratio which is acquired by the continuing partners from the retiring partner is called gain ratio. If gain ratio added to old ratio we will get New ratio. It means New ratio = Old ratio + Gain ratio by interchanging the terms, we will get Gain ratio = New ratio – Old ratio.

Question 2.

Retiring partner’s share in profit up to the date of his retirement will be debited to Profit and Loss Suspense Account.

Answer:

This statement is True.

If a partner retires from the firm during the accounting year, the profit or loss for the period from the date of last balance sheet to the date of retirement is calculated on the basis of last year’s profit or average profit and it is credited to retiring partner’s capital A/c and for time being it debited to new account called Profit and Loss Expense A/c. This is because final accounts cannot be prepared on any date during the accounting year.

Question 3.

On retirement of a partner, sacrifice ratio is considered.

Answer:

This statement is False.

On retirement of a partner, his share is acquired by continuing partners in certain proportion and it is nothing but gain for them. Therefore, on retirement of a partner instead of sacrifice ratio gain ratio is considered.

![]()

Question 4.

Retiring partner is called an outgoing partner.

Answer:

This statement is True.

When a person retires from the firm due to health issues, financial issues or personal reasons then it is known as person retires from the business and for the business, he is an outgoing partner.

Question 5.

On retirement of a partner, remaining partner will share the goodwill in their profit sharing ratio.

Answer:

This statement is False.

On retirement of a partner, after giving retiring, partner’s share in goodwill and if goodwill is written off, then remaining partners will adjust the goodwill in their new profit sharing ratio. (If raised to full extent and written off)

Question 6.

Retiring partner is not entitled to share in general reserve and accumulated profit.

Answer:

This statement is False.

General reserve and accumulated profit are created out of past undistributed profit, such profits are the outcome of hard work of all the partners including retiring partner. Hence, retiring partner’s has right to share general reserve and accumulated profit. He is therefore, entitled to get share in general reserve and accumlated profit.

D. Fill in the blanks and rewrite the following sentence:

Question 1.

New Ratio (less) ______________ = Gain ratio.

Answer:

Old ratio

Question 2.

Retiring partner’s share of goodwill is ______________ to remaining Partner’s Capital Account.

Answer:

debited

Question 3.

Revaluation A/c is also known as ______________ Account.

Answer:

Profit and Loss Adjustment

![]()

Question 4.

On retirement, the balance at a Current Account of a partner is transferred to his ______________ Account.

Answer:

Capital

Question 5.

A proportion in which the continuing partners get the share of retiring partner is known as ______________ Ratio.

Answer:

Gain

E. Answer in one sentence.

Question 1.

What is meant by Retirement of a Partner?

Answer:

Retirement of a partner refers to a process in which a partner leaves the firm or severes his relations with other partners on account of his old age, continued ill health, loss of interest in the firm, misunderstanding amongst the partners, etc.

Question 2.

What is Benefit Ratio?

Answer:

Profit sharing ratio which is acquired by the continuing partners on account of retirement or death of a partner is called Benefit Ratio or Gain Ratio.

Question 3.

What is New Ratio?

Answer:

The ratio in which profits or losses are shared by the continuing partners after retirement of a partner is called New Profit Sharing Ratio.

Question 4.

How is the amount due to the retiring partner settled?

Answer:

The amount due to a retiring partner is settled as per the terms of partnership agreement or otherwise mutually agreed upon either in lumpsum or in instalments.

![]()

Question 5.

How is Gain Ratio calculated?

Answer:

Gain ratio is calculated at the time of retirement of a partner by deducting old ratio from new ratio.

Question 6.

Why is retiring partner’s capital account credited with goodwill?

Answer:

Goodwill is an intangible assets or benefits accrued to the firm and its benefits are transferred to retiring partner’s Capital A/c by giving credit.

Practical Problems

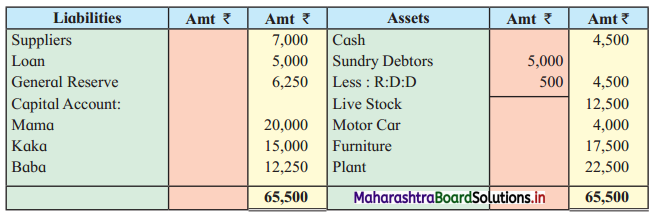

Question 1.

The Balance Sheet of Mr Mama, Kaka and Mr Baba who shared profits and losses as 4 : 3 : 3 respectively.

Balance Sheet as on 31st March, 2018

Kaka retires on 1st April, 2018 on the following terms.

1. The share of Kaka in Goodwill of the firm is valued at ₹ 2,700.

2. Furniture to be depreciated by 10% and Motor car by 12.5%.

3. Live Stock to be appreciated by 10% and Plant by 20%.

4. A provision of ₹ 2,000 to be made for a claim of compensation.

5. R.D.D. is no longer necessary.

6. The amount payable to Kaka should be transferred to his Loan A/c.

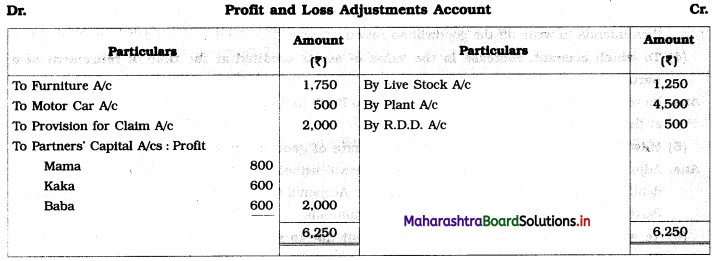

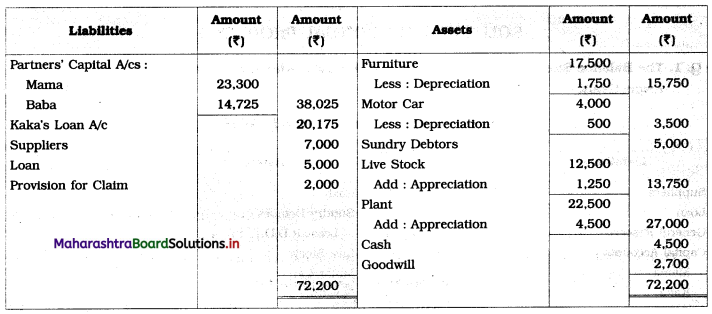

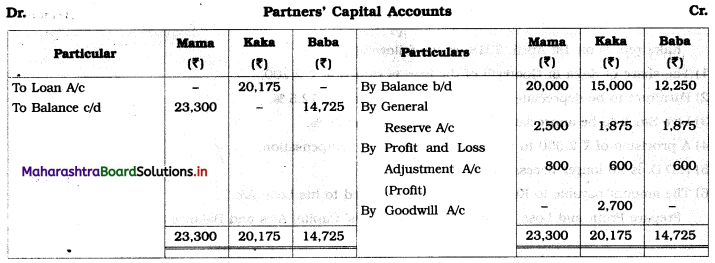

Prepare Profit and Loss Adjustment A/c, Partners’ Capital A/cs and Balance Sheet of the new firm.

Solution:

In the books of Partnership Firm

Balance Sheet as on 1st April, 2018

Working Notes:

1. R.D.D. is no longer require means it is a gain for firm.

2. A provision of ₹ 2,000 to be made for a claim of compensation, ₹ 2,000 is recorded on debit side of Profit and Loss Adjustments A/c and then on liability side of Balance Sheet.

3. Total payable amount to Kaka ₹ 20,175 is recorded as Kaka’s Loan A/c.

![]()

Question 2.

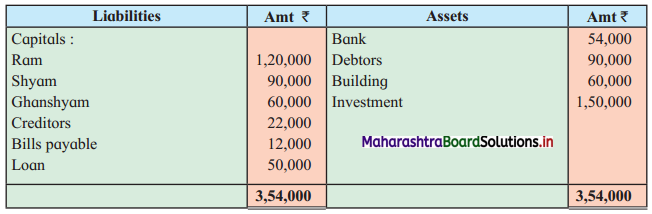

The Balance Sheet of Ram, Shyam and Ghanshyam sharing profits and losses in 3 : 2 : 1 respectively and their position on 31-3-19 were as follows:

Balance Sheet as on 31st March, 2019

Ghanshyam retired on 1st April, 2019 on the following terms:

1. Building and Investment to be appreciated by 5% and 10% respectively.

2. Provision for Doubtful Debts to be created at 5% on Debtors.

3. The provision of ₹ 3,000 be made in respect of Outstanding Salary.

4. Goodwill of the firm is valued at ₹ 90,000 and partners decide that goodwill should be written back.

5. The amount payable to the retiring partner be transferred to his Loan A/c.

Prepare: Profit and Loss Adjustment A/c, Partners’ Capital A/c, Balance Sheet of new firm.

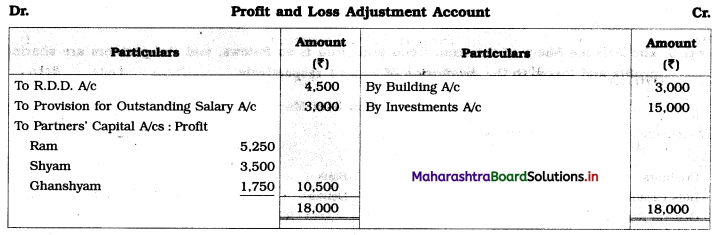

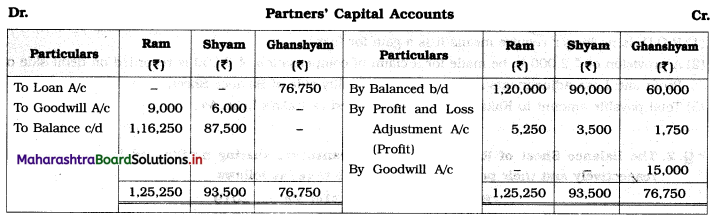

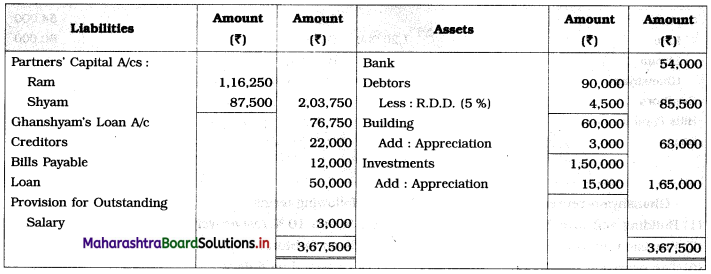

Solution:

In the books of Partnership Firm

Balance Sheet as on 1st April, 2019

Working Notes:

1. Provision of ₹ 3,000 for outstanding salary is recorded on debit side of Profit and Loss Adjustment A/c and then on the Liability side of Balance Sheet.

2. Goodwill of the firm is valued at ₹ 90,000 and share of retiring partner in it is ₹ 15,000 (\(\frac{1}{6}\)th part) and it is to be written back means it is to be shared by remaining partners in their profit-loss ratio.

Question 3.

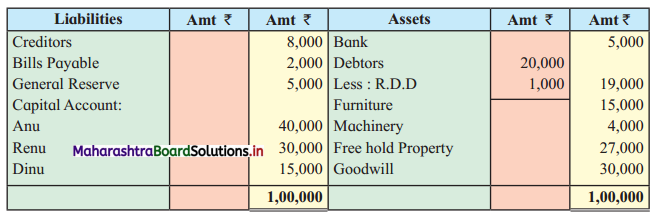

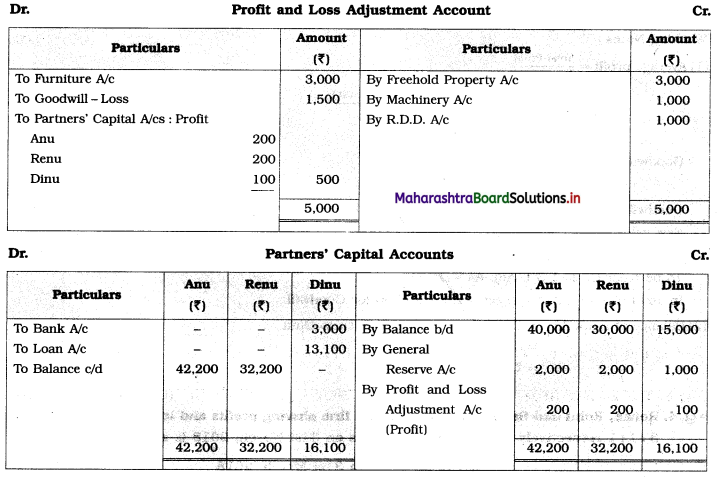

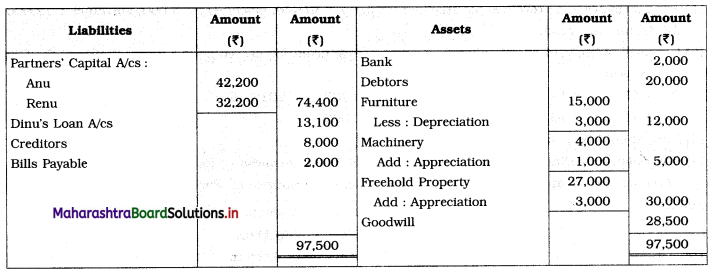

The Balance Sheet of the Anu, Renu and Dinu is as follows, and the partners are sharing profits and losses in the proportion of 2 : 2 : 1 respectively.

Balance Sheet as on 31st March, 2019

Dinu retires from the firms on 1st April, 2019 on the following terms:

1. The assets are to be revalued as : freehold property ₹ 30,000, Machinery ₹ 5,000, Furniture ₹ 12,000, All debtors are good.

2. Goodwill of the firm be valued at thrice the average profit for preceding five years. Profits of the firm for the year.

2014-15 – ₹ 14,500

2015-16 – ₹ 10,500

2016-17 – ₹ 10,000

2017-18 – ₹ 16,000

2018-19 – ₹ 10,000

3. Dinu should be paid ₹ 3,000 by cheque.

4. The Balance of Dinu’s Capital A/c should be kept in the business as loan.

Prepare: Profit and Loss Adjustment A/c, Capital Accounts of Partners, Balance Sheet of the new firm.

Solution:

In the books of Partnership Firm

Balance Sheet as on 1st April 2019

Working Notes:

1. Average profit = \(\frac{\text { Total Profit }}{\text { No. of years }}\)

= \(\frac{1000+10,500+10,000+16,000+10,000}{5}\)

= \(\frac{47,500}{5}\)

= ₹ 9,500

Goodwill = Avg. profit × No. of years

= 9,500 × 3 years

= ₹ 28,500

Goodwill value given in balance sheet = ₹ 30,000

New value arrived at = ₹ 28,500

Loss due to revaluation = ₹ 1,500

To be recorded in P & L Adj. A/c – Dr. Side.

In asset side of Balance sheet, write ₹ 28,500 for Goodwill.

2. Balance of Bank A/c = Opening Balance – Cheque given to Dinu

= 5,000 – 3,000

= ₹ 2,000

![]()

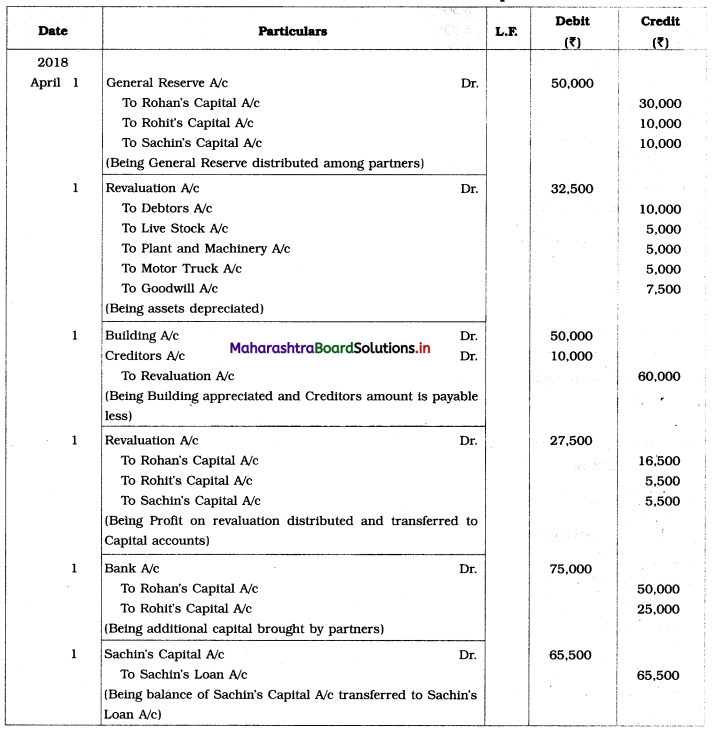

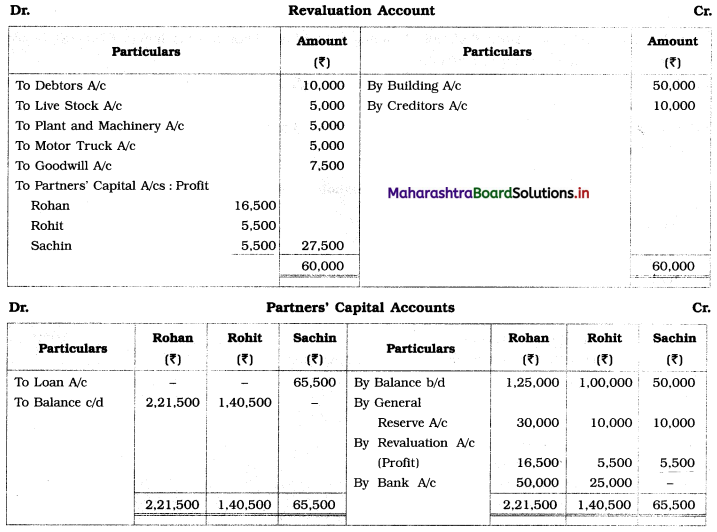

Question 4.

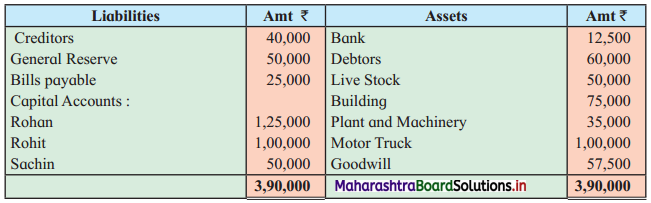

Rohan, Rohit and Sachin are partners in a firm sharing profits and losses in the proportion 3 : 1 : 1 respectively. Their balance sheet as on 31st March, 2018 is as shown below:

Balance Sheet as on 31st March, 2018

On 1st April, 2018 Sachin retired and the following adjustments have been agreed upon:

1. Goodwill was revalued on ₹ 50,000.

2. Assets and Liabilities were revalued as follows:

Debtors ₹ 50,000, Live stock ₹ 45,000, Building ₹ 1,25,000, Plant and Machinery ₹ 30,000, Motor truck ₹ 95,000 and Creditors ₹ 30,000.

3. Rohan and Rohit contributed additional capital through Net Banking of ₹ 50,000 and ₹ 25,000 respectively.

4. Balance of Sachin’s Capital Account is transferred to his Loan Account.

Give Journal entries in the books of new firm.

Solution:

Journal entries in the books of Partnership Firm

Working Notes:

1. Calculation of Profit on Revaluation of Assets and Liabilities.

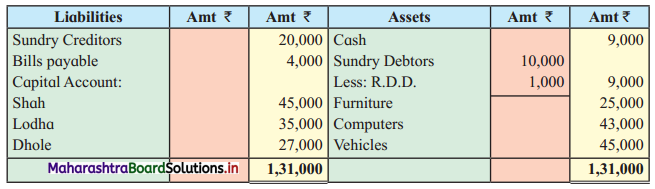

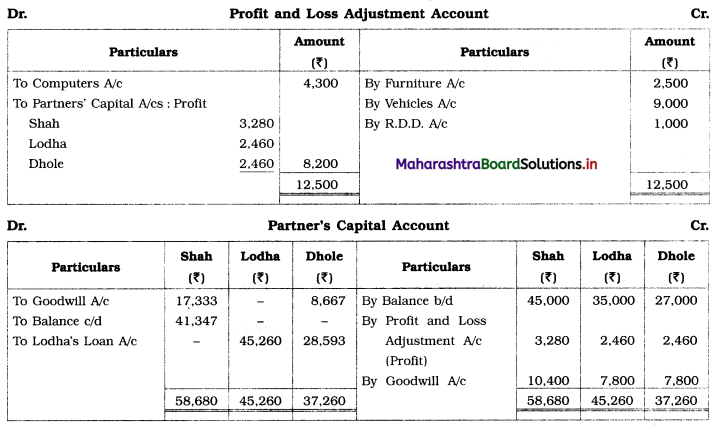

Question 5.

Shah, Lodha and Dhole were partners sharing profits and losses in the ratio of 4 : 3 : 3. Their Balance Sheet as on 31st March, 2019 is given below:

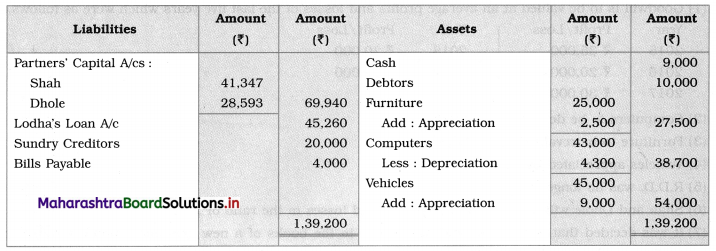

Balance Sheet as on 31st March, 2019

On 1st April, 2019 Mr. Lodha retired from the firm on the following terms:

1. Goodwill is to be valued at an average profits and losses of the last five years which were as follows:

Year – Profit/Loss

2015 – ₹ 35,000

2016 – ₹ 20,000

2017 – ₹ 30,000

2018 – ₹ 20,000

2019 – ₹ 25,000

2. Computers to be depreciated by 10%.

3. Furniture to be revalued at ₹ 27,500.

4. Vehicles appreciated by 20%.

5. R.D.D. was no longer necessary.

6. Shah and Dhole will share the future profits and losses in the ratio of 2 : 1.

7. It was decided that goodwill should not appear in the books of a new firm and amount payable to Lodha is to be transferred to his Loan A/c.

Prepare: Profit and Loss Adjustment A/c, Partners’ Capital Accounts, Balance Sheet of new firm.

Solution:

In the books of Partnership Firm

Balance Sheet as on 1st April 2019

Working Note:

Average profit = \(\frac{\text { Total Profit }}{\text { No. of Years }}\)

= \(\frac{35,000+20,000+30,000+20,000+25,000}{5}\)

= \(\frac{1,30,000}{5}\)

= ₹ 26,000

∴ Goodwill = ₹ 26,000

Goodwill should not appear in the books of accounts.

Therefore, ₹ 26,000 credited in Partners’ Capital Account in partners’ old profit and loss ratio. ₹ 26,000 will be debited in Partners’ Capital Account in partners’ new profit-loss ratio.