Balbharti Maharashtra State Board Class 8 Marathi Solutions Sulabhbharati Chapter 8 गीर्यारोहणाचा अनुभव Notes, Textbook Exercise Important Questions and Answers.

Maharashtra State Board Class 8 Marathi Solutions Chapter 8 गीर्यारोहणाचा अनुभव

Marathi Sulabhbharti Class 8 Solutions Chapter 8 गीर्यारोहणाचा अनुभव Textbook Questions and Answers

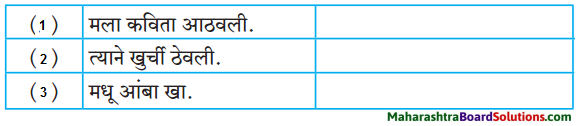

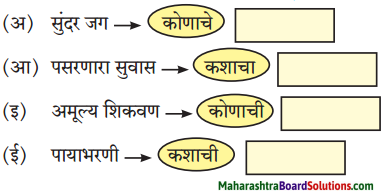

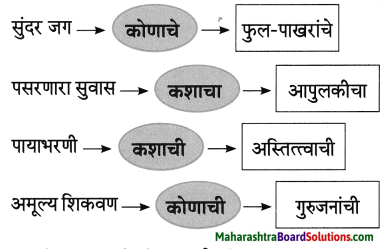

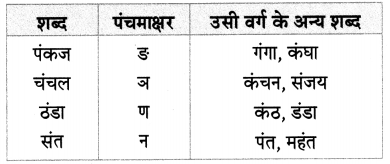

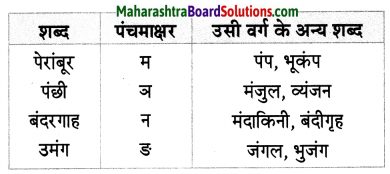

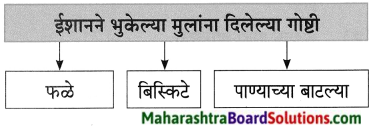

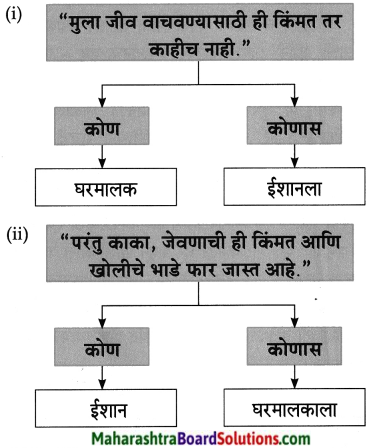

1. आकृत्या पूर्ण करा.

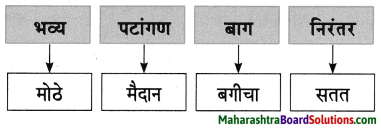

प्रश्न 1.

आकृत्या पूर्ण करा.

उत्तरः

![]()

2. एका शब्दात उत्तरे लिहा.

प्रश्न अ.

ज्या गिर्यारोहण संस्थेकडून ईशानला ई-मेल आला ते ठिकाण – []

उत्तरः

उत्तरकाशी

प्रश्न आ.

अनेक तासांच्या व थकवणाऱ्या चढाईनंतर सर्व मित्र पोहोचले ते ठिकाण – []

उत्तरः

गंगोत्री

प्रश्न इ.

बहादूरीच्या कार्यासाठी मिळणारे पदक- []

उत्तरः

वीरपदक

3. तुमच्या शब्दांत उत्तरे लिहा.

प्रश्न अ.

पाठ अभ्यासल्यानंतर तुम्हाला जाणवणारी ईशानची गुणवैशिष्ट्ये लिहा.

उत्तरः

शाळेत जाणाऱ्या ईशानला गिर्यारोहणाचा विशेष छंद होता. त्यासाठी त्याने प्रसिद्ध गिर्यारोहण संस्थेत प्रवेश घेतला. उत्कृष्ट प्रशिक्षणातून बारीक सारीक गोष्टी समजून घेतल्या होत्या. एवढ्या लहान वयात आपल्या वेड बनलेल्या छंदाचे जतन करणे व एकाग्रतेने नवीन गोष्टी शिकणे हे ईशानचे विशेष म्हणता येतील. गिर्यारोहण या प्रकारातून त्याची साहसीवृत्ती जाणवते. गंगोत्रीवर पोहोचल्यानंतर काळीज हेलावून टाकणारे दृश्य पाहून भावनिक झालेला ईशान दिसून येतो. पण दुसऱ्या क्षणी यात्रेकरूंना मदत करुन भुकेल्यांना आपल्याकडील अन्न देऊन तो मदतीच्या भावनेचे व मोठ्या मनाचे दर्शन घडवतो.

स्वत:ला भूक लागली असताना व विश्रांतीची गरज असताना देखील झाडात अडकलेल्या लोकांना वाचवून तो आपली नि:स्वार्थ वृत्ती दाखवून देतो. धूर करुन हेलिकॉप्टरला संकेत देणाऱ्या ईशानचे प्रसंगावधानही वाखाणण्याजोगे होते हे जाणवते. ईशानचे प्रसंगावधान, धैर्यशीलवृत्ती, नि:स्वार्थी, दानशूरता अशा अनेक गुणवैशिष्ट्यांचे दर्शन प्रस्तुत पाठातून घडते.

![]()

प्रश्न आ.

ईशान व त्याचे सहकारी यांनी यात्रेकरूना केलेली मदत तुमच्या शब्दांत लिहा.

उत्तरः

कठिण व थकवणाऱ्या चढाईनंतर ईशान व त्याचे मित्र गंगोत्रीला पोहोचले व त्यांच्या सहकाऱ्यांच्या नजरेस नदीचे रौद्र रूप नदीच्या वेगवान प्रवाहामुळे झालेली वित्तहानी व जीवितहानी बघून ते अडकलेल्या यात्रेकरूंच्या मदतीसाठी सरसावले. जखमी यात्रेकरूंवर मलमपट्टी करून व औषधे देऊन प्रथमोपचार केले. हरवलेल्या यात्रेकरूंचा शोध घेण्यासाठी इतर नातेवाईकांनी यात्रेकरूंची मदत केली. स्वत:च्या भुकेची पर्वा न करता स्वत:जवळ असलेला फळे, बिस्किटे व पाण्याच्या बाटल्या त्या भुकेल्या मुलांना देऊन टाकल्या. हवाईदलाचे हेलिकॉप्टर मदतीसाठी येताच ईशान व त्याच्या सहकाऱ्यांनी यात्रेकरूंना हेलिकॉप्टरपर्यंत पोहचवायला हवाईदलातील जवानांना मदत केली. त्यांनी सर्व यात्रेकरूंना नि:स्वार्थी भावनेने जमेल त्या स्वरूपात मदत केली.

प्रश्न इ.

‘कडाक्याची थंडी पडली आहे’ अशी कल्पना करून परिसरातील असाहाय्य व्यक्तीला कोणती मदत कराल ते लिहा.

उत्तरः

हिवाळा सुरू होताच थंडी हळूहळू जोर धरू लागते. स्वत:च्या घरात गोधडी घेऊन झोपल्यावरही थंडी सहन होत नाही. मात्र रस्त्यावरील असहाय्य व्यक्ती थंडीच्या दिवसातही रस्त्यावरच रात्र काढतात. अशा व्यक्तीला मी अंथरण्यासाठी एखादी चादर व अंगावर घेण्यासाठी उबदार गोधडी देईन. तसेच घरात असलेले उबदार कपड्यांपैकी स्वेटर, कान टोपी अशा गोष्टी मी त्या व्यक्तीला मदत म्हणून देईन.

खेकूया शब्दांशी.

प्रश्न अ.

खालील वाक्प्रचार व त्यांचा अर्थ यांच्या योग्य जोड्या लावा.

| ‘अ’ गट | ‘ब’ गट |

| 1. काळजाला घरे पडणे | (अ) त्रासून जाणे |

| 2. मनमानी करणे | (आ) प्रचंड दु:ख होणे |

| 3. हैराण होणे | (इ) मनाप्रमाणे वागणे |

उत्तरः

| ‘अ’ गट | ‘ब’ गट |

| 1. काळजाला घरे पडणे | (आ) प्रचंड दु:ख होणे |

| 2. मनमानी करणे | (इ) मनाप्रमाणे वागणे |

| 3. हैराण होणे | (अ) त्रासून जाणे |

![]()

प्रश्न आ.

खालील शब्दांचा वापर करुन प्रत्येकी एक वाक्य तयार करा.

उत्तरः

- गिर्यारोहण: एक साहसी, कठीण व अत्यंत कार्यक्षम खेळ म्हणून गिर्यारोहणाला विशेष महत्त्व प्राप्त झाले आहे.

- रौद्र रूप: जंगलात लागलेल्या वणव्याच्या आगीने बघता बघता रौद्र रूप धारण केले.

- भूस्खलन: भूस्खलन झाल्याने जमिनीचे रूपच पालटले.

प्रश्न इ.

‘बे’ हा उपसर्ग लावून खालील शब्द तयार करावलिहा.

उदा. – बेवारस

- जबाबदार

- इमान

- शिस्त

- रोजगार

- पर्वा

उत्तर:

- बेजबाबदार

- बेइमान

- बेशिस्त

- बेरोजगार

- बेपर्वा

![]()

प्रश्न 4.

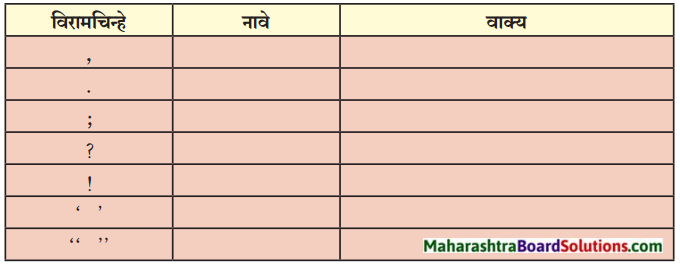

खालील तक्त्यात विरामचिन्हांची नावे लिहून, त्यांचा वापर करून वाक्य तयार करा.

उत्तर:

| विरामचिन्हे | नावे | वाक्य |

| , | स्वल्पविराम | दिवाळीसाठी लाडू, चिवडा, शंकरपाळे असा सगळा फराळ तयार असतो. |

| . | पूर्णविराम | मी आणि अनू शाळेत जातो. |

| ; | अर्धविराम | मनाला उभारी देणारा प्रवास कधी संपूच नये असे वाटते; पाहता-पाहता मैलाचे दगड मागे पडत जातात. |

| ? | प्रश्नचिन्ह | तुझी परीक्षा कधी संपणार आहे? |

| ! | उद्गारवाचक | अय्या! किती मोठी झालीस |

| ‘….’ | एकेरी अवतरण चिन्ह | कितीही मोठे झालो तरी शाळेतले ‘ते क्षण’ पुसता पुसले जात नाहीत. |

| “….” | दुहेरी अवतरण चिन्ह | बऱ्याच दिवसांनी भेटलेल्या आजीने आस्थेने विचारले, “कशी आहेस बाळा?” |

उपक्रम:

भारतातील गिर्यारोहण संस्थांबददल आंतरजालाच्या साहाय्याने माहिती मिळवा व राज्यनिहाय संस्थांच्या नावांचे तक्ते बनवा.

वाचा.

प्रश्न 1.

खालील उतारा वाचा. त्याचा तुम्हांला समजलेला अर्थ सारांश रूपाने पुन्हा लिहा.

![]()

प्रश्न 2.

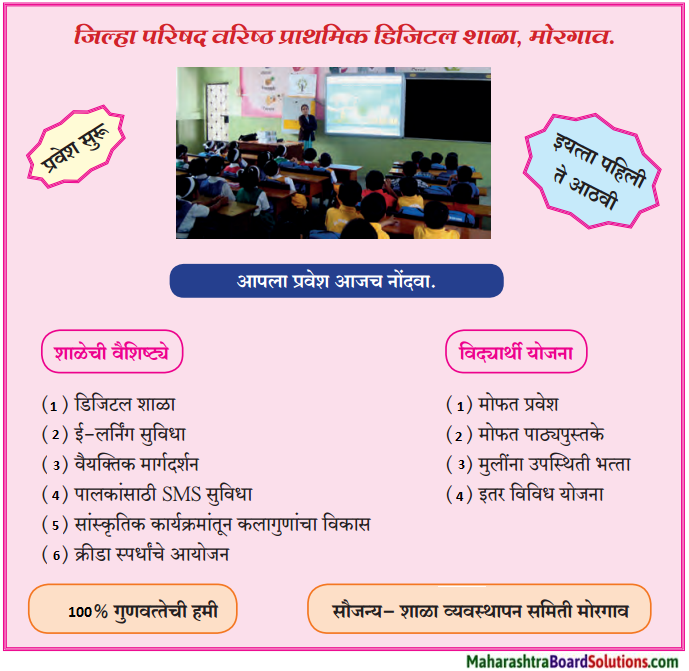

खालील जाहिरातीचे वाचन व निरीक्षण करून दिलेल्या प्रश्नांची उत्तरे लिहा.

(अ) उत्तरे लिहा.

- जाहिरातीचा विषय-

- जाहिरात देणारे (जाहिरातदार)-

- वरील जाहिरातीत सर्वांत जास्त आकर्षित करून घेणारा घटक-

- जाहिरात कोणासाठी आहे?

(आ) वरील जाहिरात अधिक आकर्षक होण्यासाठी त्यात कोणकोणत्या घटकांचा समावेश असावा, असे तुम्हांला वाटते?

(इ) तुमच्या मते जाहिरातीमधील महत्त्वाची वैशिष्ट्ये.

Class 8 Marathi Chapter 8 गीर्यारोहणाचा अनुभव Additional Important Questions and Answers

प्रश्न 1.

पुढील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

![]()

कृती 1: आकलन कृती

प्रश्न 1.

आकृतिबंध पूर्ण करा.

उत्तरः

कोण ते लिहा.

प्रश्न 1.

ईशानला पहाडावरील मोहिमेमध्ये सहभागी होण्यासाठी निमंत्रण देणारी.

उत्तरः

उत्तर काशीमधील गिर्यारोहण संस्था

प्रश्न 2.

गिर्यारोहणाचा विशेष छंद असणारा.

उत्तरः

ईशान

3. एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

ईशानला ई-मेल कोणी व का पाठवला होता?

उत्तरः

उत्तर काशीच्या गिर्यारोहण संस्थेने आपल्या एका मोहिमेमध्ये सहभागी होण्याचे निमंत्रण म्हणून ईशानला ई-मेल केला होता.

![]()

प्रश्न 2.

ईशानला गिर्यारोहण संस्थेतील प्रशिक्षणातून काय फायदा झाला होता?

उत्तरः

ईशानला गिर्यारोहण संस्थेतील प्रशिक्षणातून गिर्यारोहणातील बऱ्याच बारीकसारीक गोष्टी समजल्या होत्या.

कृती 2: आकलन कृती

प्रश्न 1.

कंसातील योग्य पर्याय वापरून रिकाम्या जागा भरा.

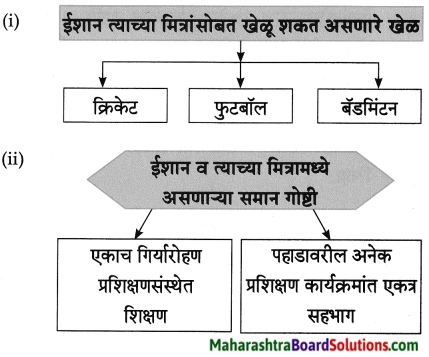

- …………… खेळून त्याला कंटाळा आला होता. (क्रिकेट, बुद्धिबळ, व्हिडिओ गेम, बॅडमिंटन)

- त्याच त्याच ……………… कथा वाचण्यात त्याला विशेष गोडी नव्हती. (साहसी, रोमांचक, गुढ, बाल)

- ………… च्या गिर्यारोहण संस्थेकडून ईशानला ई-मेल प्राप्त झाला. (उत्तरकाशी, दार्जिलिंग, पहलगाम, गुलमर्ग)

उत्तर:

- व्हिडिओ गेम

- रोमांचक

- उत्तरकाशी

प्रश्न 2.

काय घडले ते लिहा. ईशानला सुट्टी घालवण्याचा योग्य पर्याय सापडत नव्हता.

उत्तरः

ईशानला सुट्टी कशी घालवायची हा प्रश्न पडलेला असतानाच त्याला दिलासा देणारी घटना घडली. उत्तर काशीच्या गिर्यारोहण संस्थेकडून त्यांच्या एका मोहिमेत सहभागी होण्याचे निमंत्रण ईशानला ई-मेलच्या माध्यमातून मिळाले आणि तोच ई-मेल त्याच्या मित्रांना मिळाल्यामुळे गिर्यारोहणासाठी एकत्र जाण्याचा योग जुळला.

प्रश्न 3.

उत्तर दया.

ईशानने आपला गिर्यारोहणाचा छंद जपण्यासाठी काय केले?

उत्तरः

ईशानने आपला गिर्यारोहणाचा छंद जपण्यासाठी आपल्या शहरातील एका प्रसिद्ध गिर्यारोहण संस्थेत प्रवेश घेतला. तेथील उत्कृष्ट प्रशिक्षणातून त्याने गिर्यारोहणातील बऱ्याच बारीकसारीक गोष्टी समजून घेतल्या.

![]()

कृती 3: व्याकरण कृती

खालील वाक्यांतील अधोरेखित शब्दांच्या जाती ओळखा व लिहा.

प्रश्न 1.

त्याच त्याच रोमांचक कथा वाचण्यात त्याला विशेष गोडी नव्हती.

उत्तरः

रोमांचक – विशेषण, कथा – नाम, त्याला – सर्वनाम, नव्हती – क्रियापद

प्रश्न 2.

त्यांनी ईशानबरोबर पहाडावर अनेक प्रशिक्षण कार्यक्रमांत भाग घेतला होता.

उत्तरः

- त्यांनी – सर्वनाम, वर – शब्दयोगी अव्यय,

- अनेक – क्रियाविशेषण अव्यय

लेखननियमांनुसार वाक्ये पुन्हा लिहा.

प्रश्न 1.

त्याला गिर्यारोहणातील बऱ्याच बारिकसारिक गोष्टि समजल्या होत्या.

उत्तरः

त्याला गिर्यारोहणातील बऱ्याच बारीकसारीक गोष्टी समजल्या होत्या.

![]()

प्रश्न 2.

मित्रांबरोबर रोज क्रिकेट, फूटबॉल आणि बॅडमीटनही खेळता येऊ शकणार होते.

उत्तरः

मित्रांबरोबर रोज क्रिकेट, फुटबॉल आणि बॅडमिंटनही खेळता येऊ शकणार होते.

प्रश्न 3.

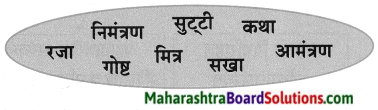

खालील शब्दांतून समानार्थी शब्दांच्या जोड्या शोधून लिहा.

उत्तरः

- सुट्टी – रजा,

- मित्र – सखा,

- कथा – गोष्ट,

- निमंत्रण – आमंत्रण.

प्रश्न 4.

खालील शब्दांचे वचन बदला.

- सुट्टी

- कथा

- घटना

- संस्था

उत्तर:

- सुट्ट्या

- कथा

- घटना

- संस्था.

कृती 4: स्वमत

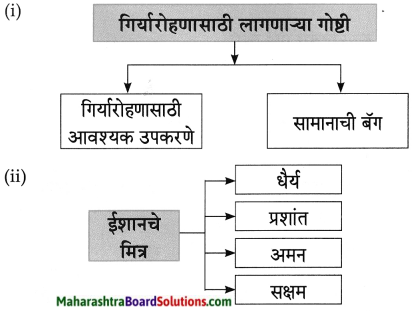

प्रश्न 1.

गिर्यारोहणाची कारणे तसेच, त्यासाठी आवश्यक गुणांची माहिती लिहा.

उत्तरः

गिर्यारोहण हा पूर्वापार चालत आलेला उत्साही आणि धाडसी गिरीप्रेमींनी जोपासलेला छंद आहे. सभोवतालच्या भौगोलिक परिस्थितीचा आढावा घेणे, शत्रूप्रदेशाची टेहाळणी करणे, हवामानविषयक अंदाज बांधणे, शास्त्रीय निरीक्षणासाठी तसेच अस्तित्वात असलेल्या हिमनदयांचा शोधघेण्यासाठी गिर्यारोहण सुरू असते. सरळसोट डोंगरकडे चढण्यासाठी गरज भासते ती प्रचंड धैर्याची, संयमाची आणि शारीरिक व मानसिक आरोग्याची. गिर्यारोहणामुळे नेतृत्व, अचूक व सत्वर निर्णयक्षमता या गुणांचा विकास होतो.

![]()

प्रश्न 2.

पुढील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

कृती 1: आकलन कृती

प्रश्न 1.

आकृतिबंध पूर्ण करा.

कंसातील योग्य पर्याय वापरून रिकाम्या जागा भरा.

प्रश्न 1.

- शाळेला सुट्टी लागल्याबरोबर सर्व मित्र …………….. ऋषिकेशहून उत्तर काशीला पोहोचले. (बसने, रेल्वेने, टॅक्सीने, सायकलने)

- वाटेत उंच उंच ……………. पाहून ते फार रोमांचित झाले होते. (पहाड, डोंगर, दऱ्या, झाडे)

- सर्व मित्रांनी मिळून माऊंटनिअरिंगच्या साहाय्याने उत्तर काशीहून …………….. ला जाण्याचा निश्चय केला. (दार्जिलिंग, पहलगाम, गंगोत्री, बद्रिनाथ)

उत्तर:

- टॅक्सीने

- पहाड

- गंगोत्री

एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

ईशान खूश का झाला?

उत्तरः

उत्तर काशीच्या गिर्यारोहण संस्थेचा संदेश वाचल्यावर ईशान खूश झाला.

प्रश्न 2.

ईशानने पहाडावर जाण्याची तयारी कधी सुरू केली?

उत्तर:

शाळेला सुट्टी लागण्यापूर्वीच ईशानने पहाडावर जाण्याची तयारी सुरू केली.

![]()

प्रश्न 3.

ईशान व त्याचे मित्र उत्साहित का झाले?

उत्तरः

गिर्यारोहण संस्थेच्या आपल्या साथीदारांना भेटल्यामुळे ईशान व त्याचे मित्र उत्साहित झाले.

कृती 2: आकलन कृती

प्रश्न 1.

खालील घटनेनंतर काय घडले ते लिहा. गिर्यारोहण संस्थेचा संदेश वाचून ईशान खूश झाला.

उत्तरः

गिर्यारोहण संस्थेचा संदेश वाचताच ईशानने त्या निमंत्रणाची माहिती आपले मित्र धैर्य, प्रशांत, अमन आणि सक्षम यांना दिली. सर्व मित्र फार खूश झाले.

प्रश्न 2.

खालील विधानामागील कारण तुमच्या शब्दांत लिहा. गिर्यारोहक आवश्यक उपकरणे व सामानाची बॅग घेऊन गिर्यारोहण करायला जातात.

उत्तरः

गिर्यारोहण हा एक साहसी प्रकार असून उंच पहाडावर प्रतिकूल परिस्थितीतही चढाई करण्याची वेळ येऊ शकते. उंच उंच दगड, निसरड्या वाटा, खोल दऱ्या यांसारखे अडथळे सुलभरित्या पार करण्यासाठी काही उपकरणांची आवश्यकता भासते. तसेच गरजेचे मात्र कमीत कमी सामान सोबत घेणे गिर्यारोहणासाठी फायदेशीर असते. यशस्वी गिर्यारोहणासाठी म्हणूनच गिर्यारोहक सामानाची व आवश्यक उपकरणांची बॅग घेऊन जातात.

प्रश्न 3.

उत्तर दया.

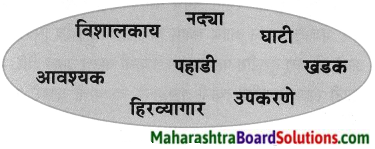

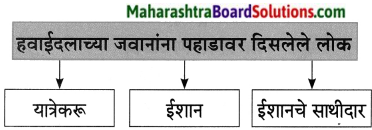

ईशान व त्याच्या साथीदारांना कोण साद घालत होते? उत्तरः गिर्यारोहण करताना दिसणारे, आकाशाला स्पर्श

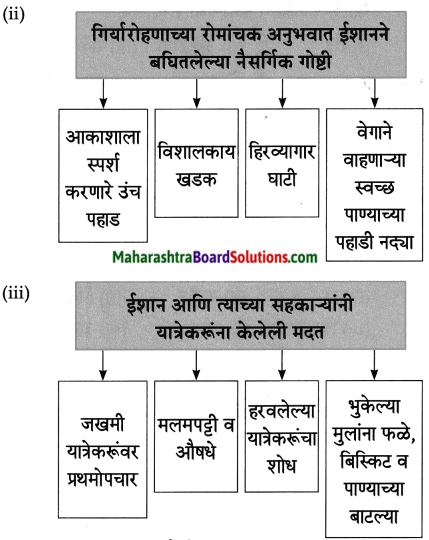

करणारे उंच पहाड, विशालकाय खडक, हिरव्यागार घाटी आणि वेगाने वाहणाऱ्या स्वच्छ पाण्याच्या पहाडी नदया, ईशान व त्याच्या साथीदारांना साद घालत होते.

![]()

कृती 3: व्याकरण कृती

प्रश्न 1.

खालील विशेषण, विशेष्याच्या जोड्या जुळवा.

उत्तर:

- विशालकाय – खडक

- पहाडी – नया

- हिरव्यागार – घाटी

- आवश्यक – उपकरणे.

प्रश्न 2.

खालील तक्ता पूर्ण करा.

उत्तर:

| शब्द | विभक्ती प्रत्यय | विभक्ती |

| पाण्याच्या | च्या | षष्ठी (अनेकवचन) |

| साथीदारांना | ना | द्वितिया (अनेकवचन) |

| सुट्टीत | त | सप्तमी (एकवचन) |

| पाहून | हून | पंचमी (एकवचन) |

प्रश्न 3.

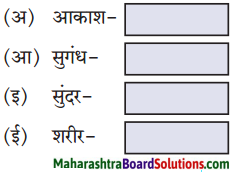

खालील शब्दांचे विरुद्धार्थी शब्द लिहा.

- स्वच्छ × [ ]

- आवश्यक × [ ]

- मित्र × [ ]

- आकाश × [ ]

उत्तर:

- अस्वच्छ

- अनावश्यक

- शत्रू

- पाताळ

![]()

प्रश्न 4.

खालील विरामचिन्हे ओळखून त्यांची नावे लिहा.

- !

- ?

- ;

- ,

उत्तर:

- ! उद्गारवाचक चिन्ह

- ? प्रश्नचिन्ह

- ; अर्धविराम

- , स्वल्पविराम

कृती 4: स्वमत

प्रश्न 1.

गिर्यारोहणाची आवश्यक उपकरणांची, सामानाची माहिती दया.

उत्तरः

गिर्यारोहण ही एक कला असून यासाठी प्रशिक्षणाची गरज असते. उत्कृष्ट प्रशिक्षण, बारकाव्यांची समज व योग्य ते सामान सोबत असल्यास गिर्यारोहण यशस्वी होऊ शकते. गिर्यारोहणासाठी उत्कृष्ट प्रतीच्या मोठ्या व दणकट सॅक आवश्यक असतात. गिर्यारोहणासाठी जाण्याच्या जागेचे तापमान, पाऊस, वारा या गोष्टींचा विचार करून योग्य तो तंबू सोबत असणे महत्त्वाचे असते. दिशादर्शक नकाशे व होकायंत्र, प्रथमोपचार पेटी, दोरी, हार्नेस, योग्य प्रकारचे बूट, गॉगल अशा अनेक गोष्टी गिर्यारोहणात महत्त्वाची भूमिका बजावतात.

पुढील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

कृती 1: आकलन कृती

प्रश्न 1.

आकृतिबंध पूर्ण करा.

उत्तरः

कंसातील योग्य पर्याय निवडून रिकाम्या जागा भरा.

प्रश्न 1.

- बरीच घरे आणि ……………….. नदीच्या वेगवान प्रवाहाबरोबर वाहून गेले होते. (मंदिरे, धर्मशाळा, गेस्ट हाऊस, शाळा)

- या तांडवात आपल्या …………… गमावल्यामुळे लोक स्फुदून स्फुदून रडत होते. (नातेवाईकांना, आप्तेष्टांना, जवळच्यांना, मित्रांना)

- ………….. झाल्यामुळे ठिकठिकाणी अनेक तीर्थयात्री अडकले होते. (भूस्खलन, भूकंप, अतिवृष्टी, ढगफुटी)

उत्तर:

- गेस्ट हाऊस

- आप्तेष्टांना

- भूस्खलन

![]()

एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

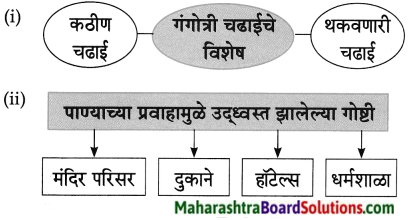

अनेक तासांच्या कठीण चढाईनंतर ईशान व त्याचे मित्र कोठे पोहचले?

उत्तरः

अनेक तासांच्या कठीण चढाईनंतर ईशान व त्याचे मित्र गंगोत्रीला पोहचले.

प्रश्न 2.

गंगोत्रीवर काय झाले होते?

उत्तरः

गंगोत्रीवर ढग अकस्मात फुटले होते व भीषण हाहाकार माजला होता.

प्रश्न 3.

लोक का रडत होते?

उत्तरः

गंगोत्रीवर झालेल्या तांडवामध्ये आपल्या आप्तेष्टांना गमावल्यामुळे लोक रडत होते.

कृती 2: आकलन कृती

प्रश्न 1.

कारणे दया. ईशान व त्याच्या साथीदारांना पहाडावरील दृश्य पाहून अंगावर काटे आले.

उत्तरः

गंगोत्रीला पोहोचल्यावर ईशान व त्याचे साथीदार खूश झाले होते. मात्र तेथील दृश्य पाहून ते हादरले. ढगफुटीमुळे गंगोत्रीवर हाहाकार माजला होता. नदीच्या वेगवान प्रवाहामुळे खूप नुकसान झाले होते. अनेकजण मृत्युमुखी पडले होते. तीर्थयात्रा करण्यासाठी आलेले यात्रेकरू अडकले होते व त्यांना सर्वस्व गमवावे लागले होते. पहाडावर हे सर्व पाहून ईशान व त्याच्या साथीदारांच्या अंगावर काटे आले.

![]()

खालील घटनेनंतर काय घडले ते लिहा.

प्रश्न 1.

पहाडामधून आलेले ढग अकस्मात फुटले.

उत्तरः

पहाडामधून आलेले ढग अकस्मात फुटल्यामुळे गंगोत्रीवर भीषण हाहाकार माजला. पाण्याच्या धोकादायक प्रवाहामुळे मंदिर परिसर, दुकाने, हॉटेल्स, धर्मशाळा उद्ध्वस्त झाल्या. बरीच घरे व गेस्ट हाऊस वाहून गेले. अनेक लोक मृत्युमुखी पडले.

प्रश्न 2.

ईशान व त्याच्या साथीदारांनी पहाडावरील भीषण तांडव पाहिले.

उत्तरः

ईशान व त्याच्या साथीदारांनी पहाडावरील भीषण तांडव पाहिले तेव्हा त्यांच्या अंगावर काटे आले व त्यांचा गिर्यारोहणाचा सर्व उत्साहच नाहिसा झाला.

उत्तर दया.

प्रश्न 1.

गंगोत्रीवरील नदीच्या तांडवाचा लोकांवर काय परिणाम झाला?

उत्तरः

गंगोत्रीवरील नदीच्या तांडवामध्ये अनेक लोकांनी आपल्या आप्तेष्टांना गमावले. अनेक तीर्थयात्री तेथे चारधाम यात्रेसाठी आले होते. मात्र भूस्खलन झाल्यामुळे सारे तीर्थयात्री ठिकठिकाणी अडकले.

![]()

कृती 3: व्याकरण कृती

खालील वाक्प्रचारांचा अर्थ सांगून वाक्यात उपयोग करा.

प्रश्न 1.

काळजाला घरे पडणे – प्रचंड दु:ख होणे.

वाक्यः अकस्मात झालेल्या भूकंपामध्ये झालेल्या जीवितहानीचा आकडा ऐकून काळजाला घरे पडली.

प्रश्न 2.

हाहाकार माजणे – घाबरून पळापळ होणे.

वाक्यः भर बाजारात सिलेंडरचा स्फोट झाल्याने सर्वत्र हाहाकार माजला.

प्रश्न 3.

अंगावर काटे येणे – प्रचंड भीती वाटणे.

वाक्य: पावसाचे चढते रौद्ररूप पाहून अंगावर काटे येत होते.

![]()

अचूक शब्द ओळखा.

प्रश्न 1.

- मुत्युमूखी, मृत्यूमुखी, मृत्युमुखी, मृत्युमुखि

- भूस्खलन, भूस्खलन, भुस्खलन, भस्खलन

- उध्वस्त, उद्ध्वस्त, उद्ध्वस्त, उद्ध्वस्त

उत्तर:

- मृत्युमुखी

- भूस्खलन

- उद्ध्वस्त

खालील शब्दसमूहासाठी एक शब्द लिहा.

- यात्रेकरूंना उतरण्यासाठीचे ठिकाण – [धर्मशाळा]

- तीर्थस्थानांना भेट देणारे लोक – [तीर्थयात्री]

- जवळील नातेवाईक – [आप्तेष्ट]

प्रश्न 1.

‘वान’ प्रत्यय लावून शब्द तयार करा. उदा. : वेगवान

उत्तरः

धनवान, गाडीवान, विदयावान, बलवान.

![]()

प्रश्न 2.

खालील शब्दांचे वचन बदला.

- पहाड

- घर

- दुकाने

- नदी

उत्तर:

- पहाड

- घरे

- दुकान

- नदया

कृती 4: स्वमत

प्रश्न 1.

ढगफुटीची माहिती दया.

उत्तर:

काही वेळा, पाऊस देणाऱ्या ढगांतून खाली आलेला पाऊस जमिनीवर न पडता जमिनीकडच्या उष्ण तापमानामुळे त्याची परत वाफ होऊन ती त्या ढगांतच सामावली जाते. ते ढग, मग तो अतिरिक्त भार घेऊन मार्गक्रमण करतात. त्यांच्या मार्गात एखादा डोंगर आल्यास त्यावर ते आदळून फुटतात. त्यामुळे, मोठ्या प्रमाणात पाऊस पडतो. त्यास ढगफुटी म्हणतात.

प्रश्न 2.

भूस्खलन म्हणजे काय?

उत्तरः

जमिनीच्या पोटातील हालचाली जसे दगड सरकणे वा पडणे, माती-खडक वाहून जाणे इत्यादी भूस्खलन या संकल्पनेतर्गत येतात. ही भूवैज्ञानिक घटना आहे. जोरदार पाऊस वा पूर किंवा भूकंप यामुळे भुस्खलन होते. त्याचप्रमाणे मानवनिर्मित कारणांमुळे, जसे झाडे, वनस्पती कापून टाकणे रस्त्याच्या कडेला असणारे डोंगर फोडणे, उंच कडा कापणे यांमुळेही ही आपत्ती ओढवू शकते.

![]()

प्रश्न 3.

पुढील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

कृती 1: आकलन कृती

प्रश्न 1.

आकृतिबंध पूर्ण करा.

उत्तरः

कंसातील योग्य पर्याय वापरून रिकाम्या जागा भरा.

प्रश्न 1.

- एका मुलाने आपल्या वडिलांकडे ……मागणी केलेली ईशानने पाहिले. (पाण्याची, बिस्किटांची, चॉकलेटची, फळांची)

- दुकानदारांची ही …………….. पाहून ईशान व त्याचे साथीदार हैराण झाले. (दादागिरी, अरेरावी, मिजास, मनमानी)

- ……………….. यात्रेकरूंचा शोध घेण्यासाठी त्यांनी मदत केली. (अडकलेल्या, भरकटलेल्या, मनमानी, हरवलेल्या)

उत्तरः

- बिस्किटांची

- मनमानी

- हरवलेल्या.

एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

हॉटेलमालक जेवणाच्या थाळीची किती किंमत वसूल करत होते?

उत्तर:

हॉटेलमालक जेवणाच्या थाळीची किंमत दोन हजार रुपये वसूल करत होते.

![]()

प्रश्न 2.

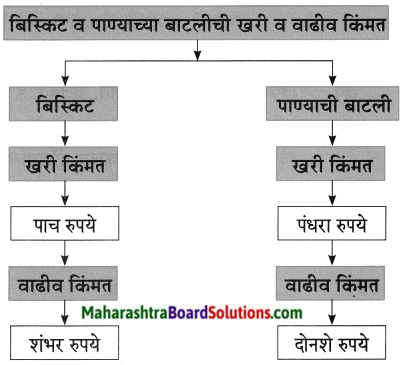

दुकानदाराने वाढीव किंमतीबाबत विचारणा केली असता काय उत्तर दिले?

उत्तर:

दुकानदाराकडे वाढीव किंमतीबाबत विचारणा केली असता तो म्हणाला की, “येथे पहाडावर वस्तू याच भावाने मिळतात ज्याला गरज वाटेल तो खरेदी करेल.”

कृती 2: आकलन कृती

प्रश्न 1.

तक्ता पूर्ण करा.

प्रश्न 2.

कोण कोणास म्हणाले ते लिहा.

उत्तरः

प्रश्न 3.

उत्तर दया.

ईशान व त्याच्या साथीदारांनी अडचणीत सापडलेल्या यात्रेकरूंना कशी मदत केली?

उत्तरः

ईशान व त्याच्या साथीदारांनी जखमी यात्रेकरूंवर प्रथमोपचार केले. त्यांची मलमपट्टी केली आणि औषधे दिली. हरवलेल्या यात्रेकरूंचा शोध घेण्यासाठी त्यांनी मदत केली. भुकेल्या मुलांना आपल्यासोबत आणलेली फळे, बिस्किटे व पाण्याच्या बाटल्या दिल्या.

![]()

प्रश्न 4.

कारणे दया. ईशान व त्याचे साथीदार हैराण झाले.

उत्तरः

पहाडावरील दुकानदार पाच रुपयांच्या बिस्किट पुढ्याची किंमत शंभर रुपये तर पंधरा रुपयांच्या पाण्याच्या बाटलीची किंमत दोनशे रुपये अशी सांगत होते. तर दुसरीकडे हॉटेल मालक जेवणाच्या थाळीची किंमत दोन हजार रुपये वसूल करत होता. दुकानदारांची ही मनमानी पाहून ईशान व त्याचे साथीदार हैराण झाले होते.

कृती 3: व्याकरण कृती

खालील वाक्यांत योग्य विरामचिन्हे घालून वाक्य पुन्हा लिहा.

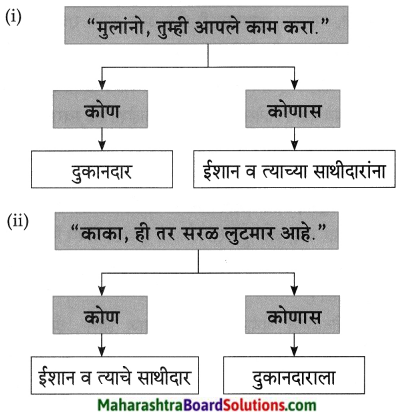

प्रश्न 1.

ज्याला गरज वाटेल तो खरेदी करेल दुकानदार रागाने म्हणाला

उत्तरः

“ज्याला गरज वाटेल, तो खरेदी करेल.” दुकानदार रागाने म्हणाला.

प्रश्न 2.

भुकेल्या मुलांना आपल्याबरोबर आणलेली फळे बिस्किटे व पाण्याच्या बाटल्या दिल्या

उत्तरः

भुकेल्या मुलांना आपल्याबरोबर आणलेली फळे, बिस्किटे व पाण्याच्या बाटल्या दिल्या.

प्रश्न 3.

काका ही तर सरळ लूटमार आहे

उत्तरः

“काका, ही तर सरळ लूटमार आहे.”

![]()

प्रश्न 4.

खालील शब्दांचे वर्गीकरण करा.

बिस्किट, दुकानदार, थाळी, किंमत, वस्तू, पहाड, यात्रेकरु, प्रथमोपचार, मलमपट्टी

उत्तरः

- पुल्लिंग स्त्रीलिंग

- नपुसकलिंग दुकानदार

- बिस्किट किंमत

- यात्रेकरू वस्तू प्रथमोपचार मलमपट्टी

- थाळी – पहाड

प्रश्न 5.

तक्ता पूर्ण करा.

उत्तरः

- शब्द मूळ शब्द सामान्यरुप दुकानदारांची दुकानदार

- दुकानदारां मुलांनो मुल – मुलां अडचणीत अडचण अडचणी

- बाटलीची बाटली बाटली

प्रश्न 6.

खालील शब्दांचे विरुद्धार्थी शब्द लिहा.

- मालक

- खरेदी

- मागणी

- राग

उत्तरे:

- नोकर

- विक्री

- पुरवठा

- लोभ, प्रेम

कृती 4: स्वमत

प्रश्न 1.

एखादया दुकानदाराने वस्तूच्या किंमतीपेक्षा जास्त पैशांची मागणी केल्यास तुम्ही काय कराल?

उत्तरः

प्रत्येक दुकानदार हा त्याच्याकडील उपलब्ध वस्तू छापील किंमतीत देण्यास बांधील असतो. मात्र कधी कधी दुकानदार वस्तूंच्या किंमती वाढवून पैसे उकळताना दिसतात. दुकानदाराने माझ्याकडे जास्त किंमतीची मागणी केल्यास मी त्याला योग्य व छापील किंमत घेण्याची विनंती करेन. त्याने न ऐकल्यास मी त्या दुकानातून वस्तू खरेदी करणार नाही व इतरांनाही त्या दुकानातून काहीही न घेण्याचा सल्ला देईन. तसेच त्या दुकानदाराची तक्रार ग्राहकमंचाकडे करीन.

![]()

पुढील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

कृती 1: आकलन कृती.

प्रश्न 1.

आकृतिबंध पूर्ण करा.

एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

दुकानदाराने जेवणाची किंमत व खोलीचे भाडे किती सांगितले?

उत्तरः

दुकानदाराने जेवणाची किंमत दहा हजार रुपये व खोलीचे भाडे पंधरा हजार रुपये सांगितले.

प्रश्न 2.

अचानक मोठा आवाज का झाला?

उत्तरः

पहाडावरील एक घर अचानक खाली कोसळल्यामुळे मोठा आवाज झाला.

![]()

प्रश्न 3.

ईशानने गिर्यारोहण संस्थेत कुठले खास प्रशिक्षण घेतले होते?

उत्तरः

ईशानने गिर्यारोहण संस्थेत पहाडावरून खाली पडलेल्या लोकांना बाहेर काढण्याचे खास प्रशिक्षण घेतले होते.

कंसातील योग्य पर्याय वापरून रिकाम्या जागा भरा.

प्रश्न 1.

- त्यांना ……….. गरज जाणवत होती. (भुकेची, पाण्याची, विश्रांतीची, झोपेची)

- ईशान व त्याचे साथीदार आपापसात …………. करत होते. (विचारविनिमय, सल्ला-मसलत, खलबत, चर्चा)

- घरात राहणारे लोक ……………… झाडात अडकले होते. (देवदारच्या, वडाच्या, अशोकाच्या, पिंपळाच्या)

उत्तरः

- विश्रांतीची

- विचारविनिमय

- देवदारच्या

कृती 2: आकलन कृती

प्रश्न 1.

कोण कोणास म्हणाले ते लिहा.

प्रश्न 2.

उत्तर दया. दुकानदाराने जेवण व खोलीचे भाडे जास्त सांगण्याचे कसे समर्थन केले?

उत्तरः

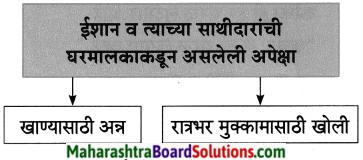

दुकानदाराने सांगितलेल्या भाड्याबद्दल ईशानने आक्षेप घेतला यावर दुकानदार म्हणाला, “जीव वाचवण्यासाठी ही किंमत तर काहीच नाही. जर भूक लागल्यावर तुम्हांला जेवण मिळाले नाही आणि रात्रभर खुल्या आकाशाखाली झोपावे लागले तर तुमचे काय हाल होतील?” अशाप्रकारे दुकानदाराने स्वत:चे समर्थन केले.

![]()

प्रश्न 3.

खालील प्रसंगानंतर काय घडले ते लिहा. घरात राहणारे लोक देवदार झाडात अडकले होते.

उत्तरः

पहाडावरील घर अचानक कोसळल्यामुळे तेथील लोक देवदारच्या झाडात अडकले. ईशानने गिर्यारोहण संस्थेत पहाडावरून खाली पडलेल्या लोकांना बाहेर काढण्याचे खास प्रशिक्षण घेतले असल्यामुळे व त्याला अशा परिस्थितीचा चांगला अनुभव असल्यामुळे ईशानने जाड व मजबूत दोराच्या साहाय्याने खाली उतरुन अडकलेल्या सर्वांना बाहेर काढले.

कृती 3: व्याकरण कृती

प्रश्न 1.

खालील शब्दांच्या जाती ओळखून त्यांचे वर्गीकरण करा. संध्याकाळ, त्यांना, थोडे, रुक्ष, म्हणाला, ईशान, ही, आवाज, कोसळले, त्याचे, देवदार, काढले, जाड, चांगला.

उत्तर:

खालील वाक्यातील अव्यये शोधा व लिहा.

प्रश्न 1.

ईशानला आता खूप भूक लागली होती.

उत्तरः

खूप – क्रियाविशेषण अव्यय

प्रश्न 2.

जेवणासाठी दहा हजार आणि खोलीचे भाडे पंधरा हजार रुपये दयावे लागेल.

उत्तरः

1. साठी – शब्दयोगी अव्यय

2. आणि – उभयान्वयी अव्यय

![]()

खालील वाक्यांतील विरामचिन्हे ओळखून त्यांची नावे लिहा.

प्रश्न 1.

“काका, आम्हांला खाण्यासाठी थोडे अन्न आणि रात्रभर मुक्काम करण्यासाठी एखादी खोली देऊ शकाल?”

उत्तर:

”…..” – दुहेरी अवतरण चिन्ह

(,) – स्वल्पविराम

(?) – प्रश्नचिन्ह

प्रश्न 2.

ईशानला अशा परिस्थितीचा चांगला अनुभव होता.

उत्तरः

(,) – पूर्णविराम

प्रश्न 3.

खालील शब्दांचे वचन बदला.

- हॉटेल

- खोली

- रुपये

- झाड

उत्तर:

- हॉटेल्स

- खोल्या

- रुपया

- झाडे

प्रश्न 4.

खालील शब्दांचे समानार्थी शब्द लिहा.

- संध्याकाळ

- रुक्ष

- घर

- आकाश

- किंमत

- पहाड

उत्तरः

- सायंकाळ

- कोरडा

- सदन, गृह

- गगन, नभ

- मूल्य

- पर्वत

![]()

कृती 4: स्वमत

प्रश्न 1.

भूकंपग्रस्त भागात तुम्ही कशाप्रकारे मदत कराल?

उत्तरः

भूकंपग्रस्त भागात झालेली मोठी हानी पाहून नडगमगता मी धीराने काम करेन. आपत्कालीन सेवा अधिकाऱ्यांच्या मार्गदर्शनाखाली जमेल तितके ढिगारे उपसायला मदत करेन. अडकलेल्या व्यक्तींना बाहेर काढण्याचा प्रयत्न करेन. जखमी लोकांना बाजूला नेऊन त्यांवर प्रथमोपचार करण्याचा प्रयत्न करेन. तसेच त्यांना वैदयकीय सेवा लवकरात लवकर मिळावी याची काळजी घेईन. तसेच भूकंपग्रस्तांना अन्नपाणी पोहोचवण्यासाठी प्रयत्नशील राहीन. मोठ्या लोकांच्या मार्गदर्शनाखाली मी जमेल तितके मदतीसाठी प्रयत्न करेन.

खालील उताऱ्याच्या आधारे दिलेल्या सूचनेनुसार कृती करा.

प्रश्न 1.

आकृतिबंध पूर्ण करा.

उत्तरः

प्रश्न 2.

कंसातील योग्य पर्याय वापरुन रिकाम्या जागा भरा.

- त्यांनी आपल्याबरोबर ……………. तंबू आणला होता. (कॉटनचा, प्लॅस्टिकचा, नायलॉनचा, कापडाचा)

- पहाडावर झालेल्या या दुर्घटनेची माहिती …………….. मिळाली होती. (सेनेला, पत्रकारांना, पोलिसांना, वृत्तवाहिन्यांना)

- हवाईदलाच्या अधिकाऱ्यांनी त्या मुलांना ………. मिळावे म्हणून राष्ट्रपतींकडे शिफारस केली. (वीरपदक, शौर्यपदक, कांस्यपदक, रौप्यपदक)

उत्तरः

- नायलॉनचा

- सेनेला

- वीरपदक

एका वाक्यात उत्तरे लिहा.

प्रश्न 1.

ईशान व त्याच्या साथीदारांची गैरसोय का झाली नाही?

उत्तरः

ईशान व त्याच्या साथीदारांना ती रात्र पहाडावर घालवावी लागणार होती. त्यांनी आपल्याबरोबर नायलॉनचा तंबू आणला होता. तो तंबू आधुनिक असल्यामुळे त्याची गैरसोय झाली नाही.

![]()

प्रश्न 2.

बचाव अभियान कोणी सुरू केले?

उत्तरः

पहाडावर झालेल्या दुर्घटनेची माहिती सेनेला मिळताच हवाईदलाच्या हेलिकॉप्टरने बचाव अभियान सुरू केले.

प्रश्न 3.

खूप धूर झाल्यामुळे काय झाले?

उत्तरः

खूप धूर झालेला पाहून हेलिकॉप्टर खाली आले व पहाडावर घिरट्या घालू लागले.

प्रश्न 4.

ईशान व त्याचे साथीदार कधी खूश झाले?

उत्तरः

ईशान व त्याचे साथीदार पहाडावर झालेल्या दुर्घटनेनंतर सुरक्षित पोहोचले, तेव्हा ते फार खूश झाले.

कृती 2: आकलन कृती.

प्रश्न 1.

कारणे दया. ईशानने व त्याच्या मित्रांनी आसपासच्या जंगलातून लाकडे गोळा करून आणली.

उत्तरः

ईशान व त्याच्या मित्रांनी गोळा करून आणलेल्या लाकडांनाआगलावली.त्यातूनखूपधूर झाला.हवाईदलाच्या हेलिकॉप्टरसाठी धूराच्या माध्यमातून संकेत देण्याचा त्यांचा हेतू होता. म्हणूनच आग लावण्यासाठी ईशान व त्याच्या मित्रांनी लाकडे गोळा करून आणली.

![]()

प्रश्न 2.

खालील प्रसंगानंतर काय घडेल ते लिहा. हवाईदलाच्या अधिकाऱ्यांना ईशान व त्याच्या साथीदारांचे बहादूरीचे कार्य समजले.

उत्तरः

हवाईदलाच्या अधिकाऱ्यांनी ईशान व त्याच्या साथीदारांचे बहादूरीचे कार्य समजताच त्यांची प्रशंसा केली. तसेच त्यांनी या मुलांना वीरपदक मिळावे म्हणून राष्ट्रपतींकडे शिफारस केली.

प्रश्न 3.

उत्तर दया. ईशान व त्याच्या साथीदारांनी केलेल्या धुरामुळे काय घडले?

उत्तरः

ईशान व त्याच्या साथीदारांनी केलेल्या धुरामुळे हवाईदलाच्या हेलिकॉप्टरला संकेत मिळाला. हेलिकॉप्टर खाली आले व पहाडावर घिरट्या घालू लागले. हवाईदलाच्या जवानांनी पहाडावर अडकलेल्या यात्रेकरूंना ईशान व त्याच्या साथीदारांना पाहिले. हेलिकॉप्टरने सर्वांना सुरक्षित

ठिकाणी पोहचवले.

कृती 3: व्याकरण कृती

प्रश्न 1.

अचूक शब्द ओळखून लिहा.

1. हेलीकॉप्टर, हेलिकॉप्टर, हेलीकॉप्टर, हेलिकोप्टर

2. आधूनिक, आधुनीक, आधुनिक, आधुनीक

उत्तर:

1. हेलिकॉप्टर

2. आधुनिक

![]()

प्रश्न 2.

‘करू’ हा प्रत्यय लावून शब्द तयार करा.

उत्तर:

1. यात्रा – यात्रेकरू

2. भाडे – भाडेकरू

प्रश्न 3.

‘निक’ हा प्रत्यय लावून शब्द तयार करा.

उदा. – आधुनिक

उत्तरः

- काल्पनिक

- रासायनिक

- भावनिक

- सपत्निक

खालील वाक्यांतील अधोरेखित शब्दांतील अव्यय ओळखून प्रकार लिहा.

प्रश्न 1.

ईशान व त्याच्या साथीदारांना ती रात्र पहाडावर घालवावी लागली.

उत्तरः

- व – उभयान्वयी अव्यय,

- ती – विशेषण,

- वर – शब्दयोगी अव्यय

प्रश्न 2.

पहाडावर झालेल्या या दुर्घटनेची माहिती सेनेला मिळाली होती.

उत्तरः

वर – शब्दयोगी अव्यय

![]()

प्रश्न 3.

खालील शब्दांचे समानार्थी शब्द लिहा.

- रात्र

- आधुनिक

- संकेत

- प्रशंसा

- बहादुरी

- मदत

उत्तर:

- निषा, रजना

- प्रगत

- खूण, इशारा

- स्तुती

- धैर्य

- सहकार्य

प्रश्न 4.

खालील शब्दांचे विरुद्धार्थी शब्द लिहा.

- दिवस

- आधुनिक

- प्रशंसा

- स्मरण

- गैरसोय

- सुरक्षित

उत्तरः

- रात्र

- प्राचीन

- निंदा

- विस्मरण

- सोय

- असुरक्षित

कृती 4: स्वमत

प्रश्न 1.

तुमच्या हातून एखादे बहादुरीचे कार्य घडले आहे का? घटना नमूद करा.

उत्तरः

अशी एक घटना आमच्या इथे घडली होती. आमच्या घरापासून काही अंतरावर एक नदी वाहते तिथे बरीच मंडळी पोहण्यासाठी, पाण्यात डुंबण्यासाठी येतात. उन्हाळ्याचे दिवस असल्याने मीही तिथे पोहायला गेलो असता, थोड्या अंतरावरुन मला एक आवाज ऐकू आला ‘वाचवा वाचवा’. मी त्या दिशेने पाहिले तर एक आठ-नऊ वर्षांचा मुलगा पाण्यात ओढला जात होता आणि त्याच्या आजूबाजूला कोणीही नव्हते.

मी क्षणाचाही विलंब न लावता पाण्यात उतरलो. पोहण्यात तरबेज असल्याने लागलीच त्याच्याजवळ पोहोचलो व त्याला बाहेर काढले. मग त्याच्या पोटातील पाणी बाहेर काढले व त्याला श्वास पुरवला. तो मुलगा शुद्धीवर आला. मला खूप आनंद झाला. त्याला घेऊन त्याच्या घरी सोडले. त्या घटनेने गावात सगळीकडे माझ्या कार्याचे, साहसाचे कौतुक झाले.

गीर्यारोहणाचा अनुभव Summary in Marathi

पाठपरिचय:

रमेश महाले लिखित ‘गिर्यारोहणाचा अनुभव’ हा पाठ अनेक रोमांचकारी घटनांनी भरला आहे. ईशान व त्याचे मित्र गिर्यारोहणासाठी गंगोत्री येथे गेले असताना ते सर्व विदयार्थी गंगोत्री येथे उद्भवलेल्या ढगफुटीच्या आणि भूस्खलनाच्या संकटातून यात्रेकरूंना मदत करून माणुसकीचे दर्शन घडवतात. या पाठातून अशा बऱ्याच गोष्टी आपणास शिकावयास मिळतात.

The lesson ‘Giryarohanacha Anubhav’ is filled with many exciting incidents. Ishan and his friends goes to the Gangotri for mountaineering. But beacuse of the crisis like cloudburst and landslide many visitors at Gangotri gets affected. Ishan and his friends help everyone to get out of these crisis and shows humanity. There are lot of things to learn through this chapter.

![]()

शब्दार्थ:

- रोमांचक – अंगावर काटे उभे करणारे – thriller,exciting

- कथा – गोष्ट – story

- गोडी – आवड – liking

- दिलासा – समाधान – assurance

- गिर्यारोहण – पर्वत चढणे/चढाई – mountaineering

- निमंत्रण – आमंत्रण – invitation

- छंद – आवड – hobby

- प्रशिक्षण – शिकवणी – training

- विशाल – खूप मोठे – huge

- घाटी – टेकडीवरील चढ असलेली लहान वाट – a hill passage with a mild ascent

- उपकरणे – साधनसामुग्री – equipments

- संदेश – निरोप – massage

- सोपे – सहज – easy

- थकवा – शीण – fatigue

- ढगफुटी – एकाएकी कोसळणारा मुसळधार पाऊस – cloudburst

- भीषण – भयानक – terrible

- धोकादायक- च्यापासून धोका आहे अशी – dangerous

- प्रवाह – वाहणे, वाहण्याचा ओघ – stream, flow

- मंदिर – देऊळ – temple

- आप्तेष्ट – जवळचे नातेवाईक – close relative

- भूस्खलन – जमीन खचणे – landslide

- तीर्थयात्री – तीर्थयात्रा करणारे – pilgrim

- प्रथमोपचार – प्राथमिक उपचार – firstaid

- रुक्ष – कोरडा – arid, dry

- खुल्या – मोकळ्या – open

- विचारविनिमय – विचारांची देवाणघेवाण – exchange of views

- संकेत – खूण, इशारा – indication, hint

- बहादुरी – धैर्य – courage

- दुर्घटना – वाईट घटना – calamity

वाक्प्रचार:

- गोडी नसणे – आवड नसणे

- प्राप्त होणे – मिळणे

- साद घालणे – हाक मारणे

- काळजाला घरे पडणे – प्रचंड दुःख होणे

- हाहाकार माजणे – घाबरून पळापळ होणे

- मृत्युमुखी पडणे – मरण पावणे

- स्फुदून स्फुदून रडणे – हुंदके देऊन रडणे

- अंगावर काटे येणे – प्रचंड भीती वाटणे

- भुकेने व्याकूळ होणे – अतिशय भूक लागल्याने अस्वस्थ होणे

- मनमानी करणे – मनाला वाटेल तसे वागणे

- हैराण होणे – त्रासून जाणे

- प्रशंसा करणे – कौतुक करणे

- शिफारस करणे – दुसऱ्याजवळ केलेली प्रशंसा

टिपा

1. गिर्यारोहण: गिर्यारोहण म्हणजे पर्वतावर चढण्याचे शास्त्र किंवा कला. एक साहसी, कठीण व अत्यंत कार्यक्षमतेचा खेळ म्हणून त्यास विशेष महत्त्व प्राप्त झाले आहे. अखिल भारतीय क्रीडामंडळानेही त्यास एक क्रीडाप्रकार म्हणून रीतसर मान्यता दिली आहे. गिर्यारोहणात दहा-पंधरा मीटर उंचीची टेकडी चढण्यापासून ते माऊंट एव्हरेस्टसारखे उंच शिखर चढण्यापर्यंतचे सर्व प्रकार येतात.

2. ढगफुटी: काही वेळा, पाऊस देणाऱ्या ढगांतून खाली आलेला पाऊस जमिनीवर न पडता, जमिनीकडच्या उष्ण तापमानामुळे त्याची परत वाफ होऊन ती त्या ढगांतच सामावली जाते. ते ढग, मग तो अतिरिक्त भार घेऊन मार्गक्रमण करतात. त्यांच्या मार्गात एखादा डोंगर आल्यास त्यावर ते आदळून फुटतात. त्यामुळे, मोठ्या प्रमाणात पाऊस पडतो. यास ढगफुटी म्हणतात. सर्वसाधारणपणे प्रतितास 100 मिली मीटर किंवा त्यापेक्षा अधिक पाऊस पडला तर ढगफुटी झाली असे मानले जाते.

3. भूस्खलन: जमिनीच्या पोटातील हालचाली जसे दगड सरकणे वा पडणे, माती खडक वाहून जाणे, इत्यादी भूस्खलन या संकल्पनेअंतर्गत येतात. ही भूवैज्ञानिक घटना आहे.

4. चारधाम यात्रा: हिंदू धर्मात चार पवित्र क्षेत्रांना चारधाम म्हटले जाते. बद्रीनाथ (उत्तराखंड), केदारनाथ (उत्तराखंड), गंगोत्री (उत्तराखंड), यमुनोत्री (उत्तराखंड) या उत्तराखंडातील धार्मिक क्षेत्रांना तसेच द्वारका (गुजरात), रामेश्वर (तामिळनाडू) व जगन्नाथपुरी (ओरिसा) या इतर तीन ठिकाणच्या धार्मिक क्षेत्रांची यात्रा म्हणजेच चारधाम यात्रा होय.

5. देवदार झाड: देवदार ही भारतात उगवणारी एक आयुर्वेदिक औषधी वनस्पती आहे. हे झाड शंकू आकाराचे असून त्याची उंची 40 ते 50 मीटर असते.

![]()